Petroleum Fiscal Systems

The petroleum industry has been one of the most profitable and strategic industries in the world since the first oil discoveries in the middle 1800s. The oil demand has been significantly increased after world war II, especially when the industrialization era began. As a result, a lot of oil industry stakeholders took this opportunity to maximize their profit.There are two major oil industry stakeholders who entitled to most of the oil exploitation profits, International Oil Companies (IOC) / contractors and government. The contractors are the company that spends huge investment and advance technologies to discover and exploit Oil and Gas (O&G) to be sold to the market. Since the O&G discoveries usually located in certain country’s regions, its government should take the benefit of the oil exploited from their region.

Although there are hundreds of petroleum fiscal system applied between contractors and governments, it could be clustered into three types of the fiscal system, namely (1) Royalty / Tax System (R/T System); (2) Production Sharing Contracts (PSC); and (3) Service Agreement. The main difference between these three fiscal systems is the government control on oil production management.

- R/T System has the least control from the government. Contractors are allowed to take full control of the O&G field operations and management, including explorations. The government will take a certain percentage of oil production as the royalty in the form of “in-kind” of “in-cash.” In-kind is the form of payment where no actual money involved; it usually in the form of goods or services. In cash is the form of payment using money as the transaction tools. While the contractors will take the remaining oil production to make profits, this system can be found in the US and some Northern Hemisphere countries.

- PSC was first introduced by Indonesia in 1966 and has been modified by many oil producer countries. PSC allowed the government to be involved in the contractor’s decision making on O&G field management by granting the contractor with cost recovery. Cost recovery is the cost that consists of operation cost, capital cost, and other costs depend on the agreement, which government will pay back to the contractor as the reimbursement. This system forces the government to be responsible for controlling and monitoring the capital and operational cost spent by the contractor.

- Service Agreement is the most controlled fiscal system by the government. This petroleum fiscal system is rarely used by countries due to its unattractive profit share for contractors. The government has full control of the O&G field and give fees to contractors to perform services on producing O&G while all the production belongs to the government. Iran is known as one of the countries that applied this petroleum fiscal system.

Regardless of the type of petroleum fiscal system implemented by the government, it is important to analyze the government takes derived from each petroleum fiscal system. The progressive petroleum fiscal system will allow the government to maximize government takes a percentage on the least cost and high oil price scenario. In other words, the government takes increase when the profit increases. However, most of the petroleum fiscal systems implemented today tend to have either neutral or even regressive characteristics. The regressive petroleum fiscal system has the opposite result with progressive system. Therefore, the percentage of government take will decrease rather in the most profitable scenario.

Generally, there are four main government take sources (extract rent) from O&G business. Each extract rent has its effect as describes below:

- Signature Bonus = Most Regressive

Signature bonuses are the amount paid to the government after the contractors obtain the legal access to operate an O&G field. It does not cost recoverable but can be tax-deductible. The difference between the signature bonus and the other bonuses is that it contains high risk since it has to be paid prior to the project start. The amount of signature bonus usually based on the bidding and negotiating procedures without proper field economics analysis. Thus, the government takes from signature bonuses will likely to fall when the field profitability increases.

- Royalty = Regressive

Royalty is one of the government taxes, which takes based on a certain percentage of the gross revenue. It can be deducted in various forms, such as % of production, fixed per unit or price deductions. Since the royalty is taken without included cost aspects, the amount of royalty will not increase when the production cost decrease.

- Taxes/profit Oil Split = Neutral

Different from royalty, taxes, and profit oil split are taken based on a certain percentage of the net revenue. It usually has neutral characteristics due to its dependency on the contractor’s net profits. However, it can also act as the progressive extract rent when there is additional sliding scale variable on the calculation.

- Government Participation = Moderately Progressive

Government participation in the project will indirectly increase government control over the O&G field operations and maintenances. It will also keep the government to get a stable government percentage in various business case scenarios. To make it more progressive, the government can add a sliding scale variable to the extract rent calculation.

History of Indonesia’s Petroleum Fiscal Systems

Before 1945, Indonesia used concession as the O&G contract form, as stated on the Indische Mijnwet. This contract model was implemented by Netherland to exploit Indonesia’s O&G resources and still be adopted by Indonesia’s government until the 1960s. Concession contract allows the government to grant the long-term contract to the contractors to explore, develop and produce O&G. Below this contract; contractors are the owner of all of the assets, the resources, and also has full authority to the field operation management including O&G sales without any government intervention. The contractors only have obligation to pay the government taxes and fees per barrel produced as compensation based on the agreement. During this contract form, government only took around 4-10% of the contractors’ gross revenue.

The second contract type applied in Indonesia was issued in 1960 in the form of a contract of work. This contract was built upon profit sharing between government and contractors. The contractors have to act as the contractor for one of Indonesia’s national oil company, namely Pertamin, Permina, and Permigan. As the contractors, they must transfer their assets to the government upon the end of the contract. The crude oil sale and distribution also should be handled by a national company. The contract of work had successfully increased government up to 60% with minimum government take is 20% of gross revenue. The contract of work only is applied by the government for six years until 1966 and replaced by Production Sharing Contract (PSC).

The first PSC was assigned between Permina and Independence Indonesian American Oil Company (IIAPCO). By implementing PSC, the government was expected to be more involved and controlled the O&G field management. The government would reimburse cost recovery, which contained various costs spent by the contractors such as production cost, development cost, and exploration cost if only contractors were successful in discovering O&G reserves to be exploited. In return for permitting the cost recovery, the contractors were required to get annual budget approval from the government. Furthermore, PSC also stated that contractors only entitled to economic right of the O&G field, while the mineral right belongs to the government and mining right belongs to the state own company. During the PSC era, the average government take was about 57% of gross revenue.

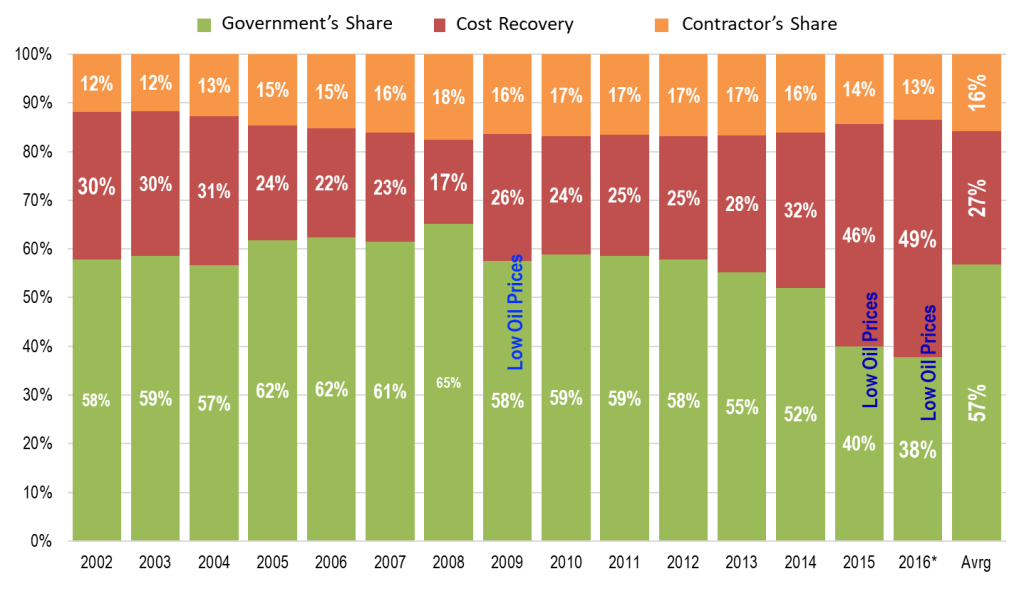

Figure 1. History of Revenue Distribution All PSC Contracts between 2000-2016 (Muin, 2018)

PSC Net Split vs. PSC Gross Split

Previously, under the PSC scheme, the government would reimburse cost recovery to the contractors, who successfully developed the O&G field. However, there were some challenges in the cost recovery implementation especially after the fallen of oil price in 2014. The sudden oil price collapsed from USD115 per barrel to under USD35 per barrel in June 2014, and it affected not only the contractors but also O&G producer countries including Indonesia. The fallen of oil price had led to significant revenue decrease to both government and contractors, while the government still had to reimburse the cost recovery, and the value was higher than its revenue, as could be seen in Figure 1. In 2016, the total cost recovery expenditure was USD11.4 billion while the government’s take was only USD9.29 billion. This deficit has put cost recovery as the source of budget pressure especially since the cost recovery is allocated from the state budget. Many believe that the high cost of cost recovery came from the inefficiency of the O&G contractors, yet the government should keep the cost as low as possible.

On the other hand, since the cost recovery is directly linked to the investment, it could also slow down the O&G exploration and development due to the low investment. Also, people still have a misperception of the cost recovery concept. It is believed that the government was giving money to the O&G contractor from the state budget rather than reimbursing the contractor for expenditure they have made to help Indonesia developing the O&G industry.

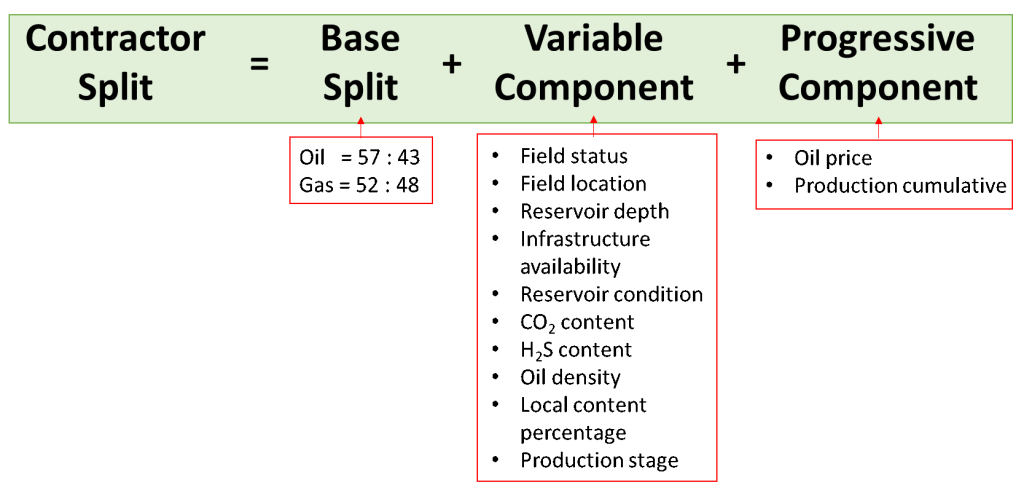

After 51 years of being implemented in Indonesia, the government finally established a new form of contract called PSC Gross Split in early 2017 under MEMR Regulation No.8 of 2017. This scheme only applied to the new or expired contracts, which will be extended. Under the PSC Gross Split, the government will no longer reimburse the cost spent by the contractors. The PSC Gross Split scheme splits the gross revenues from production between government and contractors without involving the cost components. Although the existing contracts will not be automatically adjusted to the PSC Gross Split, the contractors are allowed to request a contract scheme transition. The regulation also sets the base split percentage to be applied in every PSC Gross Split contract, and it will be adjusted based on variable component and progressive component as could be seen in Figure 2.

Figure 2. The contractor split based on PSC Gross Split

There are various reactions to the PSC Gross Split regulation, even after the new split improvement under MEMR Regulation No.52 of 2017 to increase economic attractiveness. The PSC Gross Split convinced that under this contract scheme, the government will not be required to monitor the contractor expenditure. Also, the contractor will no longer need to request annual budget approval for the government. However, since PSC Gross Split still bounded to the income tax, it is unlikely for the contractor to be exempted from the audit.

Another concern is that many experts believe that PSC Gross Split will decrease the O&G development due to its low fiscal attractiveness compared to the previous PSC Net Split. To answer this concern, the government has made economic analysis for various O&G field conditions, and the results showed that under the new PSC Gross Split, the contractor could still get higher IRR (Internal Rate of Return) and NPV (Net Present Value). The contractor can request government to adjust the split at POD (Plan of Development) and commencement of production, even though there is a polemic if Ministry of Finance should be involved in the agreement.

Is it Regressive, Neutral, or Progressive?

Regardless of the pros and cons of the PSC Gross Split implementation, it is important to know the characteristics of the fiscal system related to the government’s take. The previous PSC scheme has a neutral characteristic since the government takes based on the net revenue. It means that the lower the cost, the higher the government take percentage. In this scheme, both contractors and the government are managed to lower the expenditure so their revenue can be higher. However, if the oil price is dropped as occurred in 2014 or the costs are increasing, both government and contractor are subjected to the losses.

Under the PSC Gross Split, the government takes tend to be regressive even there is a progressive component within the split. As the government split is based on the gross revenue, it is not included the cost to the calculation similar to the royalty characteristic. The government take will increase when the production revenue increase. However, when the contractors can cut their costs, the contractor is able to increase their profit percentage. On the other hand, the government takes percentage will likely decrease.

Furthermore, the progressive component provided by the government only based on the oil price and production cumulative, as shown in Figure 2. These two components are not directly linked to the cost fluctuations. Other than production and price based, there are another two progressive components that can be implemented to accommodate the cost changing, namely “R” Factor and ROR (Rate of Return). R – Factor is directly related to the payback of the investment; it is calculated as the ratio of the cumulative revenue after-tax to cumulative expenditure including capital expenditure and operating cost. ROR is the system linked to the project’s return on investment. Both the “R” factor or ROR will allow government to increase their take based on the profit to investment ratio (P/I), although this might associate with gold plating – or a situation where contractor will spend more on unnecessary investment to adjust their NPV and IRR level.

Bibliography

- Johnston, D. (2019). Petroleum Fiscal System and Production Sharing Contracts.

- Muin, A. (2018). Krisis Harga Minyak Dunia : “Tantangan Eksplorasi & Produksi Migas Kedepan”.

- Sudibjo, R. (n.d.). PSC Gross Split. Teknik Perminyakan ITB, Bandung.

- *This opinion piece is the author(s) own and does not necessarily represent opinions of the Purnomo Yusgiantoro Center (PYC)